🏦 HOW BANKS CREATE MONEY

PAGE 1 OF 5 · A LOAN IS NEW MONEY

MORE THAN A MONEY JAR

THEY TYPE NUMBERS, AND IT COUNTS

A lot of people think a bank is only a very heavy safe that stores old notes. The surprising part: when a bank approves a loan, it can type a new balance into a screen. That fresh number in your account is money the world did not have a second ago. A big share of the money in the system started life as credit from a normal bank, not as paper from a little mint. Big picture: most money you see in apps is a digital promise, and loans are one way the pile grows.

💡 TINY TRUE FACTS

Think of a huge pile: almost all the pounds or rupees in daily life sit as numbers in bank ledgers, not as paper in a wallet. That does not make it fake for your lunch money. It means the story of money and the story of a bank are tied together in a very modern way.

CLICK

KINDS OF "MONEY"

📊 ROUGH PICTURE (UK STYLE)

💳 A very large part is bank made through lending and the flow of credit.

🪙 A small sliver is the coins and notes a central bank prints and we can touch with our hands.

🏦 The central bank is the "big ref" of the system, the commercial bank in your high street is where the daily typing happens. Adult sources such as the Bank of England have explained the split in a similar way. Exact counts change, but the shape of the story stays: digital first, then cash.

🪙 A small sliver is the coins and notes a central bank prints and we can touch with our hands.

🏦 The central bank is the "big ref" of the system, the commercial bank in your high street is where the daily typing happens. Adult sources such as the Bank of England have explained the split in a similar way. Exact counts change, but the shape of the story stays: digital first, then cash.

A BIG PHRASE

Fractional reserve means a bank is allowed to set aside only a slice of each deposit as "kept in the back room" money, and the rest can flow out as loans. Each loan is not always a handover of a single wad the bank already had; the process can create new spending power in the system. Grown up books have many footnotes, but the kid size headline is: banks, loans, and new account balances go together.

PAGE 2 OF 5 · ONE BLEEP, MANY TURNS

THE "MULTIPLIER" STORY

A DEPOSIT CAN SPARK A CHAIN

Picture a round number for learning: you stick in one thousand, the bank tucks a tenth away as the "held back" part in this toy story, and lends the rest. The person who got the loan spends, someone else takes that in as a fresh deposit, and the chain keeps going. Add up the new balances, and the total in the system can be many times the first one thousand, even though no one printed a new note for every step. Simpler words: the first saving wiggles through the banking world and the credit promise can spread. Real rules and maths are messier, but the picture is the point.

CHAIN

TURN 1

🅰️ FIRST BANK (TOY 10%)

You add 1000 on screen one.

Team A keeps a 100 slice, lends 900 out to a buyer.

The world just picked up 900 new "can spend" from a fresh loan, while your 1000 is still in the first story.

Team A keeps a 100 slice, lends 900 out to a buyer.

The world just picked up 900 new "can spend" from a fresh loan, while your 1000 is still in the first story.

TURN 2

🅱️ WHERE THE 900 SITS NOW

Team B takes in 900, keeps 90, lends 810.

Another hop, new promises, new balances, same idea until the number left to lend gets tiny. Your head can rest when the story feels clear: **many steps, not one giant coin bag in the basement**.

Another hop, new promises, new balances, same idea until the number left to lend gets tiny. Your head can rest when the story feels clear: **many steps, not one giant coin bag in the basement**.

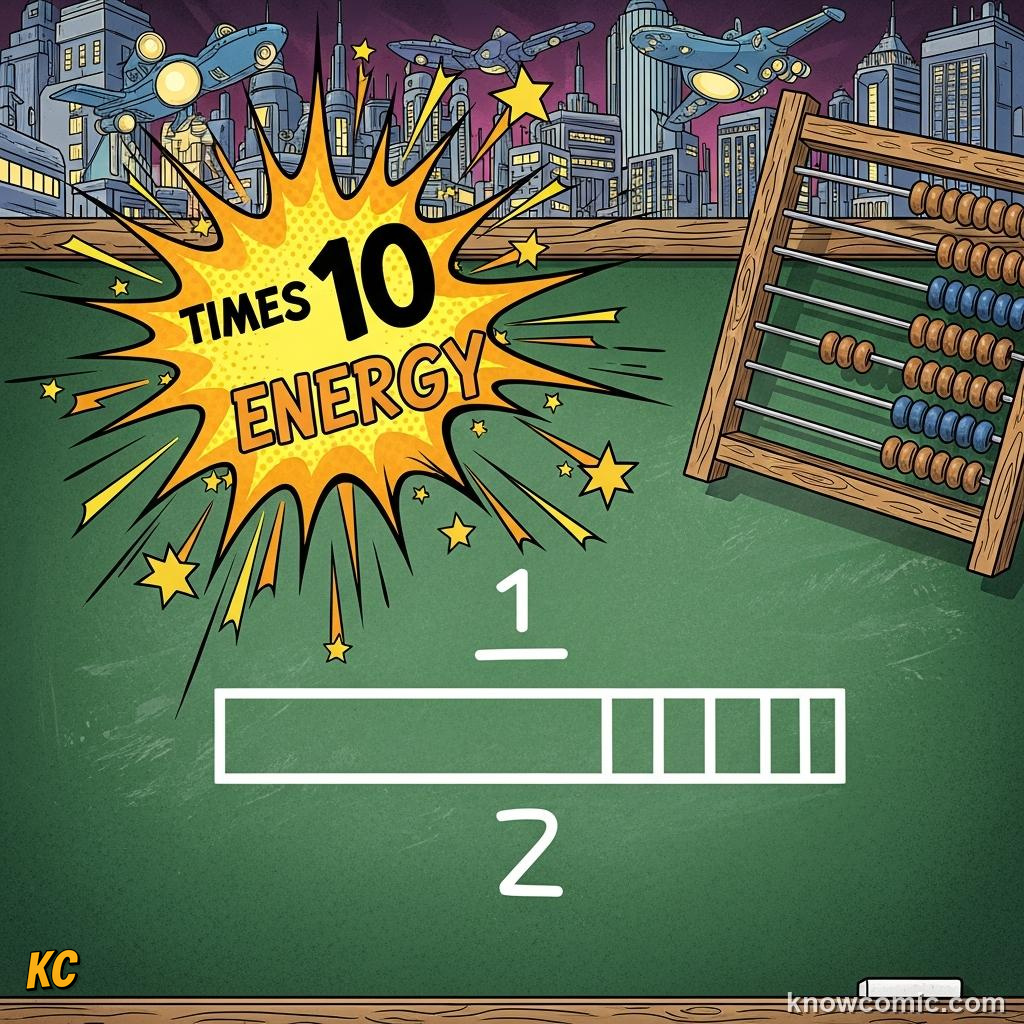

KID SIZED SUM

➗ ABOUT THAT "10X"

If you always keep a tenth, a neat old fraction trick says the total of deposits the chain can reach is about the first number times ten (one divided by point one, if you already love decimals). The real world adds brakes, grumpy days when nobody wants a loan, and rule books, but the multiplier idea is that the first "yes, save it" can start a long queue of new "yes, lend it" story lines.

PAGE 3 OF 5 · THE DIALS AND THE OOPS MOMENTS

WHEN THE CHAIN TURNS WILD

A story you might hear in the news: years like 2008, when a huge pile of housing loans went wobbly. Folks who could not pay, houses worth less, banks in trouble, grown ups in government stepping in. You do not need the whole score card yet. The kid headline is: if everyone borrows the same bet at once, a soft landing is hard.

ONE EXTRA TOOL: QE

Quantitative easing is a mouthful. Picture the central team creating fresh electronic pounds and using them to buy government IOU paper (bonds) to wake up a sleepy economy when the normal "raise or lower a loan's price" dial is already at the floor. The UK and others used it after big scares. It is not magic free candy; it is a very serious lever for adults who watch inflation all night.

THE DIALS ON THE WALL

RATES UP, SLOW BORROWING. RATES DOWN, MORE LOANS

The central bank of your country, think Bank of England or a cousin overseas, nudges a few big levers. A higher interest rate makes new loans pricier, so fewer new loans, less fresh credit, cooler spending. A lower rate does the opposite, more room for the chain we drew on the last page. The goal is a steady town: not too hot, not too cold. Grown up fights about the exact right speed never end, but you now know the basic steering wheel: cost of credit and pace of new lending are partners.

DIALS

PAGE 4 OF 5 · THE SCARY MORNING RUSH

BANK RUN

IF EVERYONE ASKS FOR CASH AT THE SAME TIME

A bank in this kind of system does not keep a separate coin for every pound on a screen. It keeps trust and a plan for enough cash for normal life. A run is when a rumour, or a true shock, makes a huge line form and everyone wants to turn the whole screen into paper right now. The building cannot do it, not because the staff are mean, but because the story was always "we will pay you over time as others pay us." When that group belief snaps, the whole game can wobble. That is why you see safety rules, insurance plans, and calm adult voices in a crisis, not just a scolding.

RUSH

TRUST IS THE FLOOR

Think of a three legged stool: the rules, the people who watch the bank, and the quiet belief in the line "your balance is there." If one leg wobbles, the chair tips fast. The economy is the same, just bigger chairs.

NOT ALL BAD NEWS

Credit also builds houses, school loans, and the shop on the corner. The job is to keep the good story of "promise and pay back" from turning into a bad story of "everyone panicked on the same Tuesday."

TELL A FRIEND

One sentence for the playground: most day to day money is a bank promise, not a coin in a sock, and a loan is how a lot of that promise is born. If they ask "is that real," you can say "it is real because the whole town acts like it is, until the trust hiccups."

PAGE 5 OF 5 · PIGGY BANK VERSUS REAL BANK

YOU, YOUR ACCOUNT, THE BIG WORLD

MONEY IN YOUR LIFE STILL COUNTS

Your allowance in a box and your balance in an app both matter for you. The wild bank stuff up here is the plumbing behind a lot of grown up plans: how a new cafe gets a start loan, how a family buys a first flat, how a school borrows to fix a roof. Good lesson for any age: a loan is a promise to pay back, the whole system is a promise to trust the promise, and a central bank nudges the "speed limit" of new promises. We keep it friendly on purpose. Later books add algebra. For now, if a younger cousin asks, you can say: "Most money is a bank story we all agree to, and new loans are one way the story grows."

🎓 LATER, IF YOU DIVE DEEPER

Older lessons spell out balance sheets, capital, shadow banks, and a hundred more labels. The KnowComic path will meet you with small steps, same voice: plain words first, then the long names.

TRUTH

TWO SAVINGS STORIES

Piggy on the desk: a coin in your hand, yours until you spend it, easy to see.

Account on the phone: a number a bank owes to you while the story says it is still there, even though the coins live in a shared cloud of promises. Both can feel "mine," the rules behind them are just different.

Account on the phone: a number a bank owes to you while the story says it is still there, even though the coins live in a shared cloud of promises. Both can feel "mine," the rules behind them are just different.

RECAP

📌 REMEMBER

✦ A loan from a normal bank can be how new spendable balances begin, not just moving one old wad in a loop.

✦ A chain of keeping a slice, lending a slice, deposit again is how a small first saving can, in a tidy textbook, line up to a much bigger pile of on screen money.

✦ Central banks twist the "price of borrowing" dial, and when that is not enough, they sometimes do very large bond buying plans called QE (grown up stress toy).

✦ A run is when the town forgets to trust, everyone asks for paper at once, the bank cannot, not because a teller is lazy, because the old story was never "every coin, every day, in this drawer for you alone."

✦ You always get to ask: who gets helped, who gets hurt, when the pipe grows fast or the pipe freezes. This topic gave you the pipe picture, kind answer first.

✦ A chain of keeping a slice, lending a slice, deposit again is how a small first saving can, in a tidy textbook, line up to a much bigger pile of on screen money.

✦ Central banks twist the "price of borrowing" dial, and when that is not enough, they sometimes do very large bond buying plans called QE (grown up stress toy).

✦ A run is when the town forgets to trust, everyone asks for paper at once, the bank cannot, not because a teller is lazy, because the old story was never "every coin, every day, in this drawer for you alone."

✦ You always get to ask: who gets helped, who gets hurt, when the pipe grows fast or the pipe freezes. This topic gave you the pipe picture, kind answer first.

🧠 QUIZ TIME!

HOW BANKS CREATE MONEY · 5 QUESTIONS

QUESTION 01

In the model grown ups use for the United Kingdom, about what share of money in the wild comes from the credit story of normal banks, not from physical notes the central bank alone prints for your pocket?

QUESTION 02

In a tidy textbook, with a 10% kept slice, if one chain starts with a 1000 pound first deposit, what is the "about" total of all deposits the chain can reach, in the smooth story?

QUESTION 03

When prices are rising too fast, what is one classic move a central bank makes to cool down new loans?

QUESTION 04

In a simple kid sentence, what is quantitative easing, also called QE?

QUESTION 05

In plain words, what is a "bank run" and why is it a problem?

0/5

LOADING...